When I take on a new client, I generally obtain 60 to 72 months of P&Ls and balance sheets.

Among the scores of metrics I review from my financial modeling system is DSO, or days sales outstanding. That number typically hovers around 30 days. My focus isn’t on the number per se. I’m looking for trends, positive or negative.

However, would you believe I have never used DSO to measure AR performance when I worked full-time as a CFO and controller in the W-2 world? DSO is somewhat useful, but I view it as a vanity metric.

The Accounts Receivable Aging Is Our Starting Point

In my last CFO job as a W-2 employee, I met with Lisa every Wednesday at 3:00 p.m. for more than one hour going over past-due accounts. We never missed a meeting. If she was out on vacation, another staff member filled in. If I was out, my accounting manager covered my absence.

Each week, for each past due, we tried to understand the underlying causes of the payment delays. Every slow-paying account had a story. Accordingly, we would strategize on how to collect those late dollars.

I was somewhat handcuffed in what I could do to prevent past-due amounts from even occurring strategically. I wanted to keep each customer’s credit card on file and use it when their account went past due. My bosses, all Board members, would not allow that.

To summarize, my focus wasn’t on DSO. It was watching the aging report like a hawk.

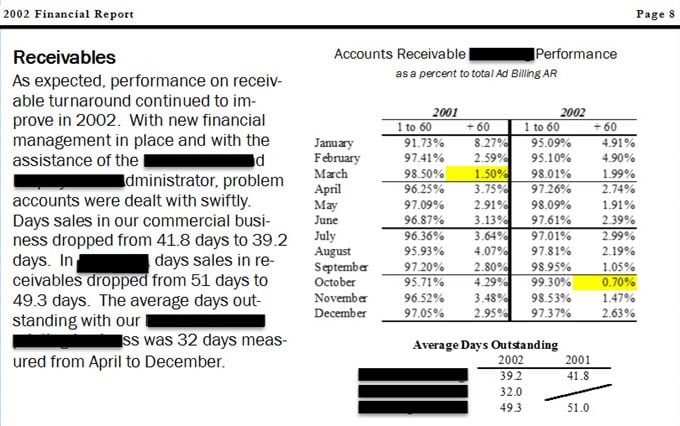

In my board report, I did report DSO (see image below). I also tracked past dues over 60 days, watching for trends, good or bad. Below is an internal report with names and departments hidden.

That experience was an eye-opener and the perfect case study on how not to manage AR. Lisa and I were doing the right work, but we were not able to prevent these problems.

DSO will not prescribe how to handle your past-due accounts. The aging schedule will alert you to who the recurring culprits are. Accordingly, here’s what I want you to do:

- Anytime a customer is one day past due, call them immediately. Don’t email them. Call them. Remind them of your payment terms. They pay late because you allow them, just like in the situation above. The Board tied my hands, so those customers mentioned above knew there were no repercussions for paying late.

- Working on past-due accounts is a downstream activity. Problems start upstream. Deal with payment issues before they occur. Sales reps need to educate customers/clients on what an invoice looks like and when it needs to be paid. I don’t think this process happens enough in small businesses.

- Start considering advance payments or automatic ACH transactions for all due dates.

A New Metric to Consider

Eli Goldratt introduced the concept of Inventory Dollar Days in his Theory of Constraints (TOC) framework. We could easily apply the same concept to past-due receivables or the entire AR portfolio.

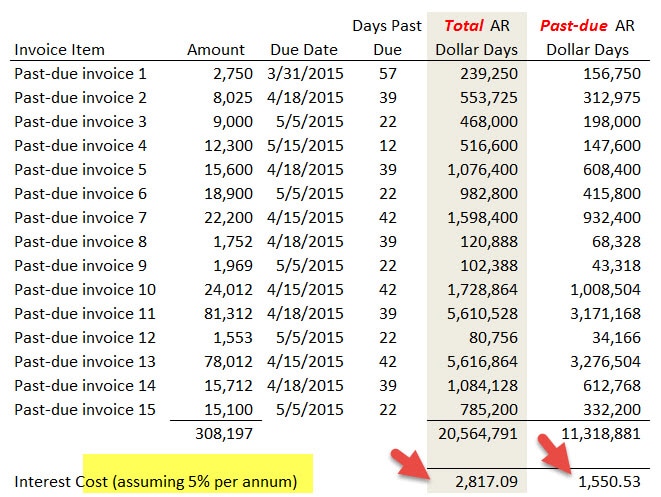

The excerpt below only shows 15 hypothetical past-due customer invoices totaling nearly $302,000. What sounds worse? Some $302,000 or more than $11,000,000 in past-due dollar days? Or better yet, how about over $21,000,000 in total AR dollar days?

AR Dollar Days Calculation:

Here’s how we calculate AR dollar days: take the customer account balance times the number of days outstanding (for example, a $2,750 invoice with 87 days outstanding equals $239,250 in AR dollar days). If the focus is primarily on past-due accounts, another option is to calculate the metric using the number of days past due. In the example above, both calculations are reflected above.

Again, you can apply the dollar days calculation to all accounts in AR–you need to find what set of numbers works best in your situation.

Questions to Ponder Relating to Your Receivables

How does your AR management measure up? Is it good? Need work? Consider the following questions and be ready to discuss them in your organization:

- Does your accounting department set aside time weekly to collect on past-due accounts? If not, why not?

- Do you put as much emphasis on an account 5 days past due as an account that is 30 days past due? Remember, an account 30 or more days past due was once just a day past due.

- Are you putting any focus on eliminating past-due accounts? Or is the focus only on collections of past-due accounts?

- What metric or flash reporting do you rely on for accounts receivable management? There’s nothing wrong with DSO reporting. DSO reporting is not the tactical reporting used for collecting those past-due accounts.