Perfectionists hate the new year.

We go crazy because we keep typing the old year into our personal finance applications.

I hate to admit this, but I still write about 4 or 5 hard-copy checks a month. Same thing is happening–I keep using the old year.

I have a solution for you. It’s not perfect, and it falls under the category of Detective/Corrective controls instead of Preventive controls. Let me explain.

This solution applies primarily for QuickBooks® users and those of you using competitive products. Entering the prior year is a tad harder to screw up in larger ERP solutions.

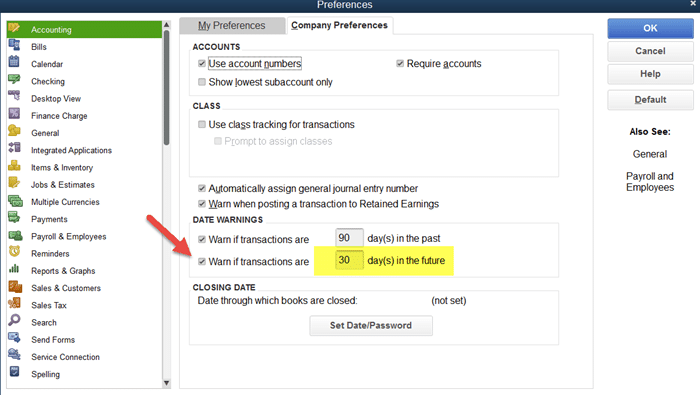

Step 1 – Consider Modifying Your Date Warnings Under Accounting Preferences

QuickBooks® allows you to password-protect dates. That is, if you password protect December 31 of any year, I need the secret word to process in that protected period. I can still post. I just need to be special and know the password you created.

That’s not the fix because every business will need about three weeks to complete their hard close. That allows every controller and accounting manager to get every vendor bill for a good/service entered into the system if it applies to the previous year. So we need to keep December open. Password protecting therefore becomes inefficient.

My suggestion? Set the warning to about 200 days or thereabouts. Why such a big number when the default is only 30 days?

We only want that warning coming up when it’s apparent we meant December 28, 2014 instead of December 28, 2015 as an example. But use your own judgement on the date warning.

Below is the screen where you will change your date setting. Look under preferences, and then find the Accounting tab.

{kind=link}

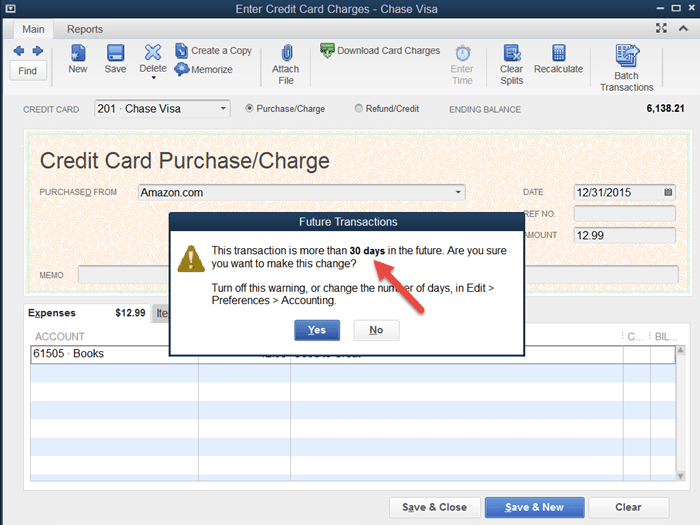

Notice the message you get when posting to a future period beyond the days you set in preferences above.

{kind=link}

The ideal solution in QuickBooks® would be to disallow transactions entered beyond a certain current date. Forget the warning. Just don’t let me post 60, 120 days out, or some other period I select.

For now, we need to follow the suggested route provided above.

Step 2 – Regularly Check Your GL for Postings 30 Days and Beyond

Earlier, I mentioned that my solution is not preventive. That is, I can’t prevent mis-postings from happening (the way I would design the preventive control).

Instead, my solution falls under the category of detective-type controls.

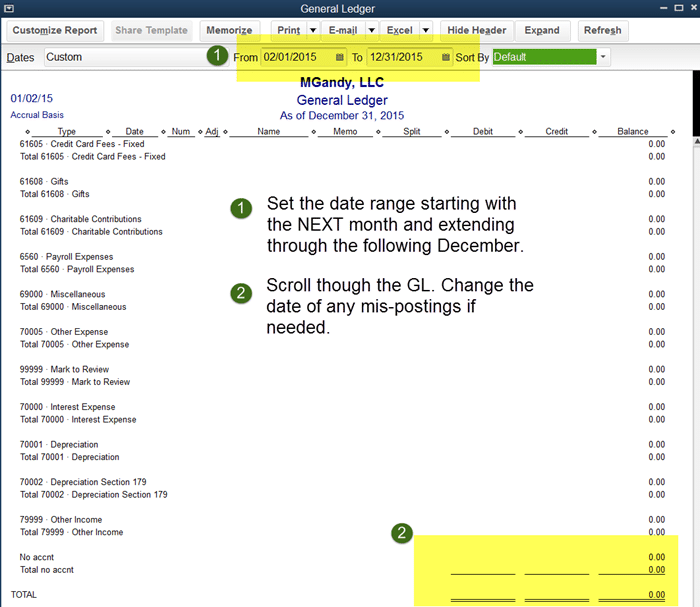

For about a three-week time period from January 1 through the next three weeks, I recommend that you run a general ledger report for a date range that starts with today and ends on December 31st of the new year.

Scroll through the repor checking for obvious mis-posting that should have been recorded in the prior year.

{kind=link}

Step 3 – Now Do a Lock Down of the Prior Year

I would then password-protect the old year by the third week of January. That three-week window gives you ample time to get every transaction recorded related to the old year.

I don’t have a problem going back to make a prior-year correction if you have not given your trial balance to the CPA firm for tax or audit purposes.

If you have already shared those files with the CPA firm, and you need to record a prior-year transaction, just make sure you provide the CPA with corrected numbers.

Now, resolve to be less of a perfectionist in the new year. But still be a likable authority (I credit that term to Copyblogger’s Sonia Simone).