In another life, I would have been a forensic accountant. I considered that career path early in my career, but a demanding travel schedule would have disrupted a stable family life. So I plowed ahead with another passion, which was small business corporate finance & operations (F&O).

Little did I know that my F&O journey would lead me to finding fraudulent activity at one of my clients. Several years ago, I discovered fraud happening right under my client’s nose, and she had no idea this was happening, despite the ongoing act being avoidable.

What was the fraud? How did I find it? How did we expose the fraudster’s deed? Did internal controls improve after I uncovered the theft?

I Wasn’t Smart, I Was Lucky

When I start work on any small business, I have three pillars that are my constant focus as an F&O executive:

- Product/business health and vitality (is the product or product family thriving, flailing, or somewhere in between?)

- Operational excellence – typically a forgone conclusion in my line of work. However, my focus is on holistic organizational collaboration, with a mindset of continually striving to improve in the eyes of our customers.

- Marketing – the two most important jobs of any business are finding a customer and then serving a customer. Finding is hard and is typically relegated to a flavor of the month and executed by a me-too marketing agency that claims their process will work (and that is rare). Show me a great marketing mindset in the small business, and then we can end the dreadful strategic planning exercises each year.

In short, the product, operational excellence, and marketing are the critical drivers of long-term sustainability in any business. Financial performance, financial competence, and economic knowledge are essential, but they don’t drive the cash flow we need and want. Instead, the three pillars do.

Once I review the business I’m working on under these three pillar lenses, then we can start modeling or quantifying the key activities in terms of units and dollars. And that’s where this story begins.

How A Financial Methodology Revealed Fraud

If product vitality, operational excellence, and smart marketing are the key drivers of a rock-solid cash flow, where do financial tools come into play?

In every business, I model the way a company creates, delivers, and captures value. The job to be done revolves around a few questions in no particular order:

- How much money can the owner withdraw from the business over the following year without straining the balance sheet?

- Can we afford one of several large initiatives without putting the business at risk of bankruptcy?

- Can we add the two or three new positions we need to improve and grow the business? How long will the company support the new hires before they are fully supporting the business?

- If our debt picture is more than 3x of current operating cash flow, will the next 12-18 months show improved balance sheet health?

- If we do nothing to improve the top line, what does cash look like in different scenarios where costs are increasing from 3 to 5 percent?

Modeling a business serves multiple purposes, such as answering the simple questions above. More importantly, business modeling slows the game of business down, where the owner can see how all the parts fit together (finding a customer, getting a customer, and serving a customer). They see the whole instead of the individual parts.

In short, a well-defined business model is a great teacher of small business economic management for CEOs and their leadership teams.

However, let’s return to the issue at hand — fraud. How did a simple business model reveal fraud? I discovered fraud purely by accident while building our business model. Let me explain.

The FTE Model

“Hi Amber, can you help me out with some numbers this morning?”

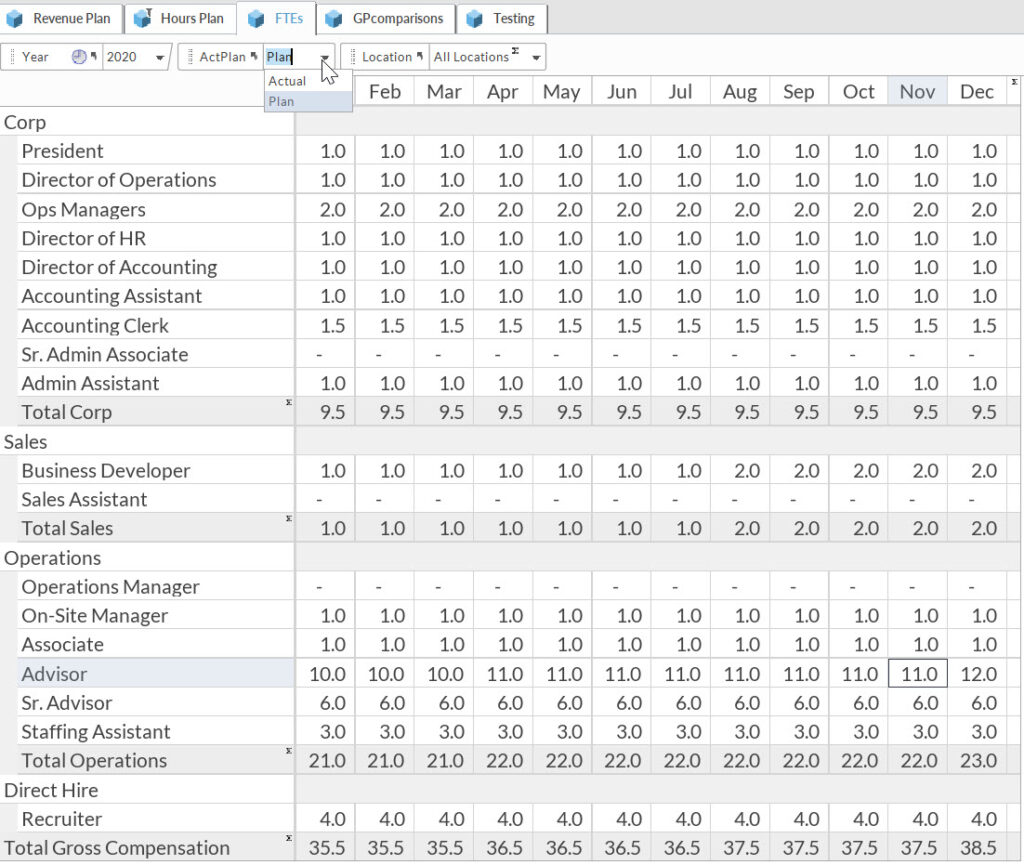

Amber is the owner of a temporary staffing agency that generates approximately $13 million in revenue per year. We had blocked out two hours to review the FTE planning model for the upcoming year. When I plugged my laptop into her large wall-mounted TV, this was our starting point:

“Amber, let’s open up your payroll system, and let’s go through the salaries for each person,” I explained. I had already programmed the commissions into my model, so I was only interested in current salaries, along with any pay raises.

The process went quickly, but the model was designed in a way that allowed for plug-and-play functionality, which further accelerated the process. That is, until we got to the controller.

“Amber, what’s wrong?”

Silence.

“Amber?”

“Mark, this isn’t right. The controller doesn’t make this much money,” said Amber.

Let’s pause here. What do you think happened? If you don’t know, that’s okay because you are missing some facts. The controller managed the payroll process from start to finish, including her hours and pay rate for each employee. Additionally, there was no oversight or a second set of eyes to review the weekly payroll before it was processed. Had the controller doubled her salary, no one would have known. But that’s not what the controller did.

Instead, the controller was padding overtime hours to her weekly pay. Since her work was unsupervised, it went undetected.

Let’s do a quick review. Amber hires a business improvement expert. The business improvement expert builds a simple model. The thinking behind the model reveals potential fraud. Accordingly, we were fortunate in uncovering this wrongdoing.

Payroll Fraud Was Not the Only Indiscretion We Found

The day before my FTE planning meeting with Amber, I was reviewing the company’s balance sheet and noticed employee payment cards, and there were about a dozen. Out of curiosity, I checked to see if the cards had been reconciled.

The answer was no. And that’s not a red flag in my world. The reconciliation issue is often due to a lack of understanding and insufficient effort on the part of the accounting staff. Other work gets in the way, and financial excellence never starts with the controller but with the owner. However, many small business owners are unaware of what financial excellence entails. Hence, many cash-like accounts rarely get reconciled (the same is true for recurring withholding and balance sheet accrual accounts).

When I shared this with the controller, she said she’d look into it. There were no facial expressions to indicate she was worried. One week later, Amber and I would find out her conscience was probably eating her up.

The Delicate Nature of Revealing Fraud

I’m not an expert in fraud detection. I’m not even sure a good TV show could have spelled out how to get the culprit to confess their sins. So I let my gut lead my thinking.

“Amber, call your labor attorney, and give her the facts.” Payroll processing occurred the following week, so we didn’t need to modify our controls, as I didn’t want the head accountant to know we were on to her just yet.

Three days later, I got a call from Amber while I was working with a craft brewing CEO. I did something I rarely do while in another meeting with a business owner — I took the call.

“Mark, it’s Amber. The controller just confessed.”

“How?” I asked.

Amber explained that the controller started getting nervous when I brought up the unreconciled employee purchasing cards. She was sure I’d begin to investigate many of the purchases (I didn’t because I was not there to conduct a fraud audit). That’s when Amber confronted her about falsifying her overtime hours. She confessed to that, too.

Amber fired her on the spot. We did not sue her, and we did not report her to local authorities. I think we should have, but you can ask me why in a private conversation.

My goal had always been for the controller to confess to her wrongful deeds before we exposed her. That happened, but I had no idea the process would unfold so quickly.

What I Learned About Fraud in Small Business

This was not my first rodeo regarding theft, but it was the first time I discovered it by accident and witnessed its ultimate conclusion with the offender confessing.

Here are a few of my takeaways:

- No owner thinks they will be a victim of theft. Amber still finds it hard to believe someone stole from her until I remind her that zero controls were in place.

- Audits will never capture theft. Theft is usually found by accident. Some fraud can continue for years, but typically, a breakdown in the fraudster’s process occurs, and the scheme is uncovered.

- Many accountants lack the skills to recommend good internal controls to prevent fraud. I’m not your person to suggest fraud-detection controls. I know the basics, but my mind is not as swift and competent as a thief.

Finally, consider hiring a forensic accountant to review your internal controls and ensure they are effective. They are far better at identifying internal control weaknesses than large auditing firms.

And that leads to my last recommendation, which is also a takeaway. Fully understand what the fraud triangle is. To learn more, check out my interview with Tiffany Couch, who wrote the very readable book, The Thief In Your Company.