“Mark, can we get the bank to go interest only for a few months?” Or “I need the money for this expansion project. Think they will loan me the money?” Finally, “I’m acquiring a competitor. I’ll get the bank to loan me the money. Can we do that?”

I’ve been a portfolio CFO since 2001 and get variations of these questions regularly. That’s because many business owners think their bank is an investor. Blanket statements are dangerous. However, the next time you have lunch with your banker, quiz them on this topic. They will agree with the sentiments I express in the paragraphs that follow.

The Mindset of a Banker

Let’s get to the point and not mince words. Here’s what your banker is thinking in the context of loaning money to you:

- They assume you are a grown-up business that knows how to find, get, and serve customers. They assume you can handle the simple basics of money management.

- They want to be paid back based on the terms of the note agreement.

- They expect to be paid on time every month.

- They never want to collect collateral to satisfy an open loan balance.

- Overall, their goal is to reduce risk on any loan as much as possible.

Not getting paid keeps bankers up at night. They worry about it more than growing their loan portfolio. Both are important, but they want your loan paid back without hiccups.

The Mindset of a Business Owner

David Keller is a retired bank president in Missouri. I loved hearing him discuss the 5 Cs of Credit or Banking (cash flow, capital, capacity, character, and condition). David was great at telling stories about some of these key concepts of issuing bank credit. Accordingly, David should be writing this section.

Now that we understand the 5 Cs let’s look at these from the perspective of a business owner:

- They want the banker to believe in their cash flow forecasts no matter how unrealistic they appear.

- They tend to ignore their capital resources, hoping the banker will overlook what they lack (plenty of capital).

- They want to convince the banker of their capacity to grow and thrive so they will never refuse a loan request (refer to the first point above).

- They want the banker to consider their character more than the numbers that will support and service the loan.

What does the owner want? Capital. They want low barriers and resistance to financial capital through bank loans. Accordingly, their mindset is wishful thinking unless their banking acumen is firm and deep.

Is it wrong for a business owner to have the above mindset? Absolutely not, but it’s based on a lack of knowledge of how bank financing works.

Let’s start with one of the Cs in bank loans: collateral.

The Way Bankers Think About Collateral

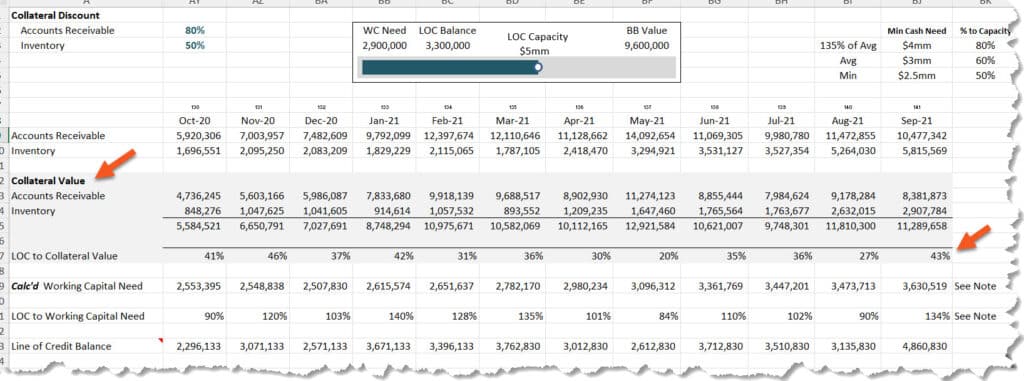

When I open a CEO’s financial statement, I’ll find a page on their balance sheet that looks something like this:

You do not need to understand the report. But notice the section on collateral value. During this 12-month look back, my client experienced a collateral-to-loan value ranging from 20 percent to 40+ percent. That was by design, as we carefully monitored the usage of our line of credit.

To summarize, a bank will discount the following assets on your balance sheet, which represents the maximum amount they will loan you:

- Receivables from customers: generally around 80 percent on ‘good’ receivables

- Inventory: generally, 50 percent on products that are movable and not obsolete

- Furniture/Fixtures/Equipment: generally about 50% of the original cost

The discount rate will be higher on vehicle fleets where a market exists, and comp values are readily available. Your list above may even include the cash value of a life policy if it’s part of the collateral. If so, there is typically no discount on that asset.

I like to address collateral value because it’s the best way to eliminate the banker-investor mindset. A business need requiring capital can only be partially funded by banking means. The rest has to be generated internally from the owner or other/new investors. A banker is not an investor but merely a lender who is confident they will get their principal back.

Character is King, Not Supreme

One of the 5 Cs of credit or bank lending is character. As David (above) would say. “Bad character will get you nowhere. Good character gets you in the door.”

What he’s saying is that good character is not enough for a banker to say ‘yes’ to a new loan, an extension, or a request to revise the loan terms. The CEO needs to prove the business model can generate enough cash flow at least 1.2 times the loan payment (that should be the minimum). For a healthy company, that multiple is around 2.0 times. High-growth companies are around 1.1 to 1.3 times the loan payment.

A CEO making an ‘ask’ of a banker needs to reveal a business model that can more than offset the principal and interest payments of a new or existing loan. That includes revealing a strong marketing, sales, and operations plan.

Accordingly, the well-intentioned CEO can rest on his/her good character for bank financing. The CEO needs to demonstrate a business model that generates positive cash flow with the capacity to keep growing and thriving.

What I Want from a CEO

I started this discussion by saying that a banker is not an investor. Let’s bookend my thoughts with the mindset I want from every CEO regarding capital:

- Again, a banker is not an investor. They manage and protect risk and want to be paid back.

- Never be a beggar in front of banks. Be clear and decisive with a bank/capital need, but do so in an innovative financial model backed by metrics showing marketing, sales, and operations excellence.

- Don’t let your problems become the bank’s problems.

Regarding that last point, capital reserves suffer when a business model fails to take hold in the marketplace. When this happens, the CEO starts stressing and uses their lender as a backstop to cash flow problems. This means they are transferring their issues to the bank. That’s not right.

There’s nothing wrong with asking a bank for breathing room as needed (think about your business situation during the COVID shutdown). However, always have a Plan B and C when borrowing money. IT HAS TO BE PAID BACK.

Bank borrowing is a tool for financing a business, but not 100 percent of it. You are the investor, not the bank. The bank is the lender, that’s all.