I’ve been mentoring and coaching CEOs as their 1099 CFO and Controller since 2001. And here’s a question I can bank on after our 128th meeting–“Mark, can you explain that cash flow statement again?”

Let’s start with a simple multiple-choice question:

Which of the following statements is generally true with respect to cash flow statements?

A. Most CEOs do not understand a cash flow statement.

B. Most CEOs focus primarily on sales, gross margins, and the bottom line.

C. Most CEOs are confused about why cash is tight when earnings are strong.

D. In the budgeting process, most CEOs do not budget/forecast working capital, CapEx, and other key components of the balance sheet.

E. All of the above.

If you selected F, then kudos (hint–that means none of the above). You are a unique CEO (as in maybe your name is Dave Kellogg). But I don’t see F. Instead, did you select E? Then read on.

Let’s Take a Look at a Streamlined Cash Flow Statement

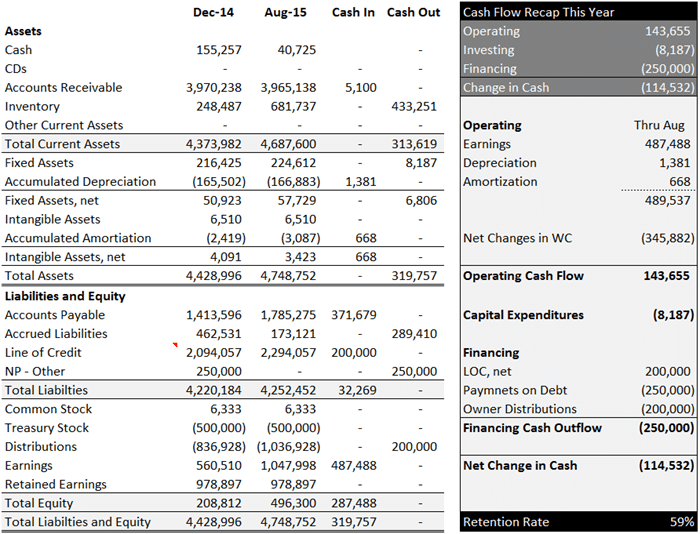

I generally create 5 to 7 views of the cash flow statements for my clients. However, the presentation below is always Page 1 of the cash flow section. Take a look at it, and ask yourself, what resonates?

{kind=link}

Our topic is Retention Rate, so let’s keep the focus there as there’s a lot going on in this simple one-pager above.

In the company above, the owner is retaining 59% of his accrual-based earnings in the business through the first 8 months of the year. The 59% retention is merely the reciprocal of this owner’s distribution rate of 41% ($200,000 divided by $487,488).

But I don’t stop here. The Retention Rate gives me clarity on how the owner is handling cash. Accordingly, there’s another important step.

In the business above, the owner and I always forecast our cash flow 12 months out every single month. So in the case above, I expect our retention rate to dip around 30% as we gain more clarity on our income tax liability, and as we true-up that estimated liability later in the year (even for s-corporation owners, we accrue owner distributions at year-end, and yes, this is GAAP).

The Retention Rate Is One of the First Key Numbers I Look at Before Accepting a New Client

Every 1099 CFO (or CEO growth coach) has his or her way of qualifying a new client. Some use benchmarking reports to present to their prospects. Others may go through a canned PowerPoint presentation.

But I obtain up to 72 months of balance sheets and income statements. And one of the first numbers I tend to study is the retention rate over time. Why? Why do I do this?

I won’t say his last name, but I answered this question recently when visiting with a brilliant entrepreneur named Mike who is nailing it with his marketing and selling efforts along with delivering an over-the-top service to his customers.

I told him, “Mike, this number helps me to understand the financial maturity of the owner I’m dealing with.” When the number is low, I know I’m dealing with a business owner whose needs and wants for cash on a personal level far outweigh the cash requirements of the business he/she is running. And that’s scary. I typically don’t take those clients on because there is a behavioral issue I’ll never be able to cure.

Can a retention rate be too high? Of course. But that’s where coaching and mentoring come into play and then prioritizing how excess cash/earnings will be deployed in the future.

That’s a good problem to have. Most of my clients with high retention rates still remember 2008-2009, and fear is motivating them to maintain higher on-hand cash levels.

What Is a Good Retention Rate?

My name is Mark Gandy, not Jim Collins. In other words, I don’t have Jim’s large research team at my disposal.

But looking through the lens of street smarts, I generally like a retention rate of:

1. Current year net margin (let’s assume 8.5% before taxes as I generally work with s-corporations), plus

2. A blend of the current and future year growth rates (let’s assume a modest 12%), plus

3. A decent margin of safety (I like 15% to 20%–I know, that’s high, but I can live with 10% too if I trust the CEO’s financial acumen).

So in the scenario above, we want to be retaining roughly 35.5% to 40.5% of our accrual-based earnings.

What does this buy us? For one, peace of mind and some margin of safety for the growing business. Academically, it means we shouldn’t be having to bring in owner capital or new term debt to fund the growth. (Editor’s note: does it now make sense why you need that new building loan when the new infrastructure will increase your asset base by more than 100%?).

Notice I didn’t say you’ll not be increasing your LOC. Your LOC will move in tandem with your receivables and inventory balances. And throughout the year, that line will be hitting zero as it yo-yos upward and downward over a 12-month period.

Instead, we’re talking new, permanent-like capital requirements when growth rates far exceed the retention rate. If sales are growing 20% and your retention rate is just 10%, you’ll need new financial capital to fund the growth.

Based on my simple premise above, I take exception to the authors who say 10% is the new bottom-line break-even point. You can be a 10% bottom-line company and still be hemorrhaging with cash flow problems.

I’ve worked with successful owners whose business models dictated a 5% bottom-line margin. They can still be successful when they are properly managing the balance sheet as closely as they are their earnings and customer success deliverables.

Figuring a retention rate is not just a scientific exercise. They key is knowing your cash requirements 6, 9, or 12 months out and giving yourself some margin for error. But in the end, your projected cash flow requirement as revealed by your cash flow model will closely mirror the methodology I presented above.

Retention Rates – For Accountants Only

I love meaningful financial statements. I hope you do too.

So please consider accruing for owner and tax distributions at year-end. Heck, I’ve even had accountants back-date the final tax distribution in March or early April retroactive to the previous December 31. And don’t worry, that journal entry is compliant with GAAP.

Let me explain what I mean with a story.

Several years ago, I was working with a successful specialty contractor. Then the 2008-2009 recession hit. For a couple years, they had no taxable earnings. Then, business started coming back in 2012 in a big way.

During the year, there were no earnings nor tax distributions to the s-corporation owner even though the cash pile was starting to get bigger. They wound up with a tax bill of around $350,000 due in April 2013. Our company bookkeeper made the payment and debited distributions in the process.

What did that do to our retention rate in 2013? It got worse as we started making some earnings distributions later in the same calendar year. In short, the 2013 retention rate became a meaningless number.

Accordingly, it’s okay to book an accrual for an estimated owner’s earnings or tax distribution (yes, they are the same, I just like to differentiate the two types of distributions). Again, this is even GAAP. It’s not financial statement re-engineering.

Finally, please don’t close out your distributions to retained earnings. I’m betting 99% of all small CPA firms do this. I hate this practice, and I’d know they’d quit this foolishness if they were responsible for reporting cash flows in 5 to 7 gyrations like every small business should.

When distributions are closed out to retained earnings, the math starts getting ugly when calculating distributons for the trailing 12 months for any month other than December.

Please don’t close out your distributions account. Keep it intact. You can thank me later when you start incorporating cash flows in your financial statements.

Retention Rates – For Open Book Management (OBM) Companies Only

I like subtleties, especially when it comes to teaching important financial concepts.

If you work in or manage an OBM company and employees own a piece of the action, here are a few suggestions that are closely related to your company’s retention rate:

1. Don’t just focus on the P&L. When I work with 10x business owners, we focus as much on the balance sheet and cash flow as we do on the P&L. One is not more important than the other. We look at the reporting as a whole. And this holistic view is not just for the senior management team–this holistic view is for everyone.

2. Don’t just focus on the here and now. Budget-centric businesses tend to put more focus on the current year P&L and resulting budget variances than they do into projected cash and debt levels 12 months out.

Let’s unpack this idea with a simple framework I’ve observed over the years. CEOs live in three different states of time as such:

a. The Past State – in this state, the CEO is focusing on what has happened (think financial statements),

b. The Current State – in this state, the CEO is focusing on what’s happening right now (think your cascaded driver-based strategic scorecard), and

c. The Future State – in this state, the typical CEO is spending tons of time playing the what-if game for scores of scenarios floating around in his/her head.

Based on the time states where CEOs live, doesn’t it make sense to be planning ahead? For the company that goes through the financials every month, part 2 of the meeting agenda should include doing some simple stress testing of key assumptions to see where cash will be one year out.

And you don’t even need to be elaborate–keep it simple like the model excerpt below.

3. Similar to my point above, be willing to sacrifice one or two years for 5 to 6 really great years in the foreseeable future. That’s what owners do. And if you have a piece of the action, that’s ownership thinking at its highest.

If your focus is just on this year and a decent year-end payout, then that’s nothing more than being part of an entitlement system. And that’s not ownership thinking. Remember, CEOs think in the past, the current, and future state. Where do they spend most of their thoughts? Your thinking should be similar.

And you do that by looking at your numbers holistically, understanding the demands placed on cash, and how it’s being retained in the company and ultimately re-invested.

A Few Parting Words

We started with Retention Rate. And in the end, you see what happens in the mind and actions of a CFO working with his amazing clients.

Those two little numbers that give us a retention rate lead to multiple strategic by-products. Once we start fixing our cash issues which may be due in part to excess owner distributions or depressed earnings, then we can start addressing cash optimization strategies and tactics. From there? It gets really interesting for the 10x CEO.

Blog Notes

I use the term 10x CEOs a lot in my writing and in my conversations with CEOs. What is a 10x CEO? I’ll answer that by saying every CEO should be listening to 10xtalk.com by Joe Polish and Dan Sullivan.

Furthermore, at the risk of shameless promotion, I highly recommend my earlier post on ROAM (Return on Assets Managed). Thinking about and understanding our Retention Rate is all about holistic financial thinking. And so is the concept of ROAM–the smaller the business, the more important this concept is, because smaller business owners have a hard time mastering the key drivers and disciplines that drive a healthly ROAM.