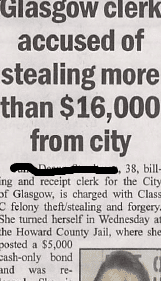

I continue to be bothered about a theft I read about in my small local paper several months ago. In brief, a court clerk admitted to forgery and embezzlement amounting to more than $16,000 in a small Missouri town.

As a former KPMG alum, I know this theft could have been detected early had some basic internal controls been in place.

How about preventable? Certainly, with the proper controls established and tested periodically.

My Search for Experts on Small Business Theft

And what does a CFO do in some of his spare time when he’s bothered by such events like embezzlement? Start finding answers from the best and brightest through Google searches.

Paydirt. I found several great articles by Ruth King at HVACR Business® on employee embezzlement. Ruth writes in an easy-to-understand language with simple follow-up strategies. I was so impressed with her writing that I reached out to her for some questions.

7 Important Questions on Employee Theft Prevention

{kind=link}

G3CFO: Ruth, you have several blog posts at HVACR Business® that every business owner should read with respect to employee theft (links to the articles are listed below). For the smaller firm generating upwards of $1 million in revenue, what is the best advice you can give to the owner to help prevent embezzlement or loss of assets of any kind?

Ruth King: Get a weekly cash flow report and send your bank statements home. Look at them each month. If they are sent electronically, look at them when you receive the emails. Don’t ignore cash. If you suspect something, say something [such as], “Can you explain this?” Don’t necessarily accuse.

You, as the owner, are the only one who can sign checks. Bookkeepers can’t sign checks. When you get a check to sign, look at the backup–purchase order, invoice, proof that the materials/services were received.

G3CFO: Is there one method or activity that is your favorite for keeping theft at bay?

Ruth King: Yes. Send your bank statements home. It is the first line of defense for embezzlement.

G3CFO: My client base ranges from $10 to roughly $90 million. Getting the owners to scan bank statements each month or online is something they normally do not want to do. Segregation of duties in these cases is then imperative, right?

Ruth King: It is their business. They can delegate the responsibility for cash flow management but they cannot abdicate it. Not looking at bank statements is abdicating your responsibilities as an owner. It takes less than 15 minutes a month. Everyone can and should invest 15 minutes a month to review cash.

G3CFO: If you had to play the role of a fraud investigator for several months for businesses ranging from $1 to $20 million in revenues, what audit steps would you perform in each business?

Ruth King: First, beginning inventory plus purchases minus ending inventory should equal the cost of goods sold. If it doesn’t, you have a problem.

Next, make sure your accounts receivable aging matches the value on the balance sheet. Make sure the accounts payable aging detail matches the value on the balance sheet.

Then, review all vendors. Ensure there aren’t near duplicates (e.g. ABC Inc. and ABC Corp.).

Finally, make sure the bank statements balance.

G3CFO: And that leads to another question. While prevention is always better than detection, should this business owner still find a way to have these audit steps performed periodically from 2 to 4 times per year?

Ruth King: If a business owner reviews financial statements each month and reviews a weekly cash flow report each week, then he should be attuned to minor changes and can spot them, thus taking care of them before they become major crises.

{kind=link}

Audit steps will be performed once a year if audited financial statements are required or as needed if financial statements and cash flow reports are reviewed as they should be.

G3CFO: A court clerk admitted to misappropriating more than $16,000 from the city of Glasgow (Missouri). It appears much of the theft was tied to cash deposits. I fault the City as it appears internal controls were either lacking or not applied. Regarding cash handling activities (currency and coin), in today’s highly technical environment, what are your favorite controls to keep such activities from happening?

Ruth King: The cash needs to be tied to the payment of receivables. Someone must review the receivables and check the bank deposits against the cash receivable payments. Also, getting a weekly cash flow report takes care of this issue too. The person receiving the cash should never prepare/make the bank deposits. When making a bank deposit, copy all deposited items and attach the copy to the deposit slip received from the bank. (This includes copying the cash to be deposited).

G3CFO: In one of your articles, you raise the sobering fact that fellow owners and partners can and do steal from one another. What is your best advice with multi-owner firms where one or more principals have cash-handling responsibilities?

Ruth King: No signature stamps. If two signatures are required, then they must be real signatures. Monthly financial review meetings with the multi-owners to analyze the financial statements [are a must]. They do trend analyses and can spot issues quickly. Also, the same principles as above apply–the person who receives cash doesn’t make bank deposits.

If one of the partners makes large purchases (boats, cars, etc.) and it looks suspicious where the money came from to make those purchases, the other partners should start digging.

G3CFO: Ruth, many thanks for your insights on this topic.

Additional Resources

Employee Embezzlement Series by Ruth King at HVACR Business®:

Protect Yourself Against Employee Embezzlement

Keep Your Money Safe

Prevent Employee Embezzlement, Part 3

Prevent Employee Embezzlement, Part 4

Books by Ruth King:

The Courage to be Profitable

The Ugly Truth about Small Business

The Ugly Truth about Managing People

Ruth King Biography

Profitability Master Ruth King is a serial entrepreneur, having owned 7 businesses in the past 30 years. One of her businesses helps small business owners understand and profit from their financial statements.

After twelve years on the road, she found a better way to reach entrepreneurs who wanted to build their businesses. She began internet training in 1998 and began the first online television-like broadcasting in 2002. Her latest channel, www.profitabilityrevolution.com, broadcasts ideas, news, strategies, and other information that matters to small business owners 24-7-365 on any internet device, mobile or laptop.

Ruth started the Decatur, Georgia, branch of the Small Business Development Center. She also founded the Women’s Entrepreneurial Center and taught a year-long course for women who wanted to start their businesses.

Ruth holds an MBA in Finance from Georgia State University.

Ruth’s best-selling book, The Courage to be Profitable, is preceded by two award-winning books, The Ugly Truth about Small Business and The Ugly Truth about Managing People.