My very first client was a small one. We did a little over $1 million in professional services. And since I quickly learned that business inside and out, we had financials completed by the first day of the month. That meant the closing was done on the last day of the month. We exceeded the goal of getting financial statements in 3 to 5 days.

Yes, it was hard. Just because the top line was small, the procedures for closing the general ledger are similar to that of a $20 or $50 million firm.

Not only were the financials closed the night of the final day of the month, but I also created a 25- to 30-page in-depth financial report. We knew exactly where we were and how and why we got there. My presentation also sketched out the future over 6 to 12 months.

Contrast the above to the typical business owner I meet who wants to hire me. On average, they are lucky to get their financials within three weeks. Even when they do, they were generated through a quick button push in QuickBooks with no analysis. They are still in the dark about their three-week-old financials.

There is a simple solution to this accounting and reporting dilemma. It starts with a checklist; financial statements can be ready in 3 to 5 days.

The Secret to Quick Numbers

I can describe the month-end close in two sentences. The financial closing begins with a complete reconciliation of the balance sheet. The financial close ends with an analytical review of the income statement. There’s more, but that’s the heart of the process as described in the video below:

We Need More than Speed, We Need Accuracy

First, do it right. Then speed it up.

Charlie Francis, Ben Johnson’s track coach, from the book Speed Trap

Timely financials are meaningless if the numbers are not accurate. Most accountants perform a bank reconciliation at a minimum, but even that process is usually completed with limitations and issues.

In most cases, I’ll find in-transit items older than 90 days. When I ask why these still exist, the typical response is, “I need to check into that.” This is called going through the motions without knowing the principles behind each step in the closing process.

Accuracy begins at the inception of every single transaction. At month’s end, we validate what we know should already be 95 to 99 percent accurate before we start the closing process.

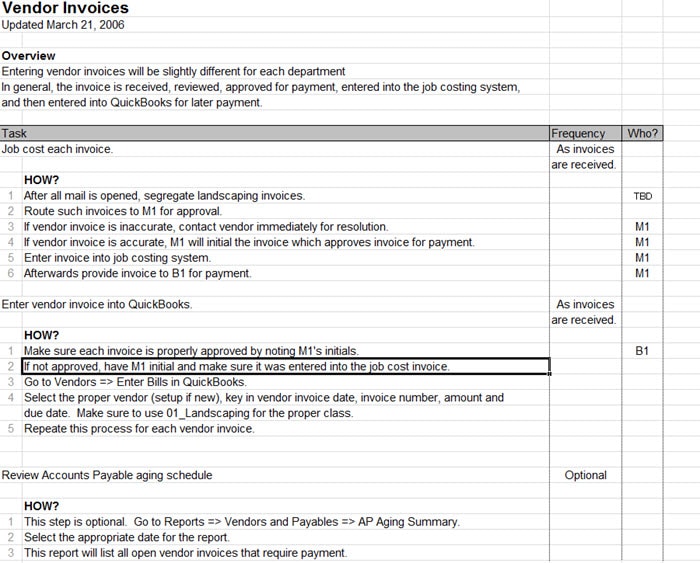

For each major transaction cycle (an example of a transaction cycle would be customer billings), I encourage accounting departments to document every step in the process. Many businesses get caught up in the proper way to document. It doesn’t matter. It just needs to be readable and repeatable. Just document. Worry about the format later.

The example below shows a pattern I follow for documenting key processes in the accounting and finance department. Notice that year, 2006. The checklist still looks the same even though we might do this today in Smartsheet, SmartSuite, Notion, or another online tool.

{kind=link}

Meaningful Financial Statements

Once we have timely and accurate numbers, we need numbers that make sense.

In my opinion, QuickBooks has done more to dumb down the financial intelligence of any accounting package I’ve encountered. Okay, that’s not fair. Instead, no accounting system publishes numbers that are easy to read.

Yet, most accounting and finance departments use push-button financial statements. Push a button, and just like that, we have canned financials for everyone to read.

I have served several magazine publishers as their Free Agent CFO™. I have asked them if anyone would read their beautiful publications if we stripped out the pictures and the graphics and turned the layout into non-formatted text only. Even though content is king, presentation is queen.

The analogy applies to financial reporting. Layout and presentation are important. And I’m not talking about eye candy filled with meaningless dashboards. The numbers need to be presented so that they tell a story. More details should follow on subsequent pages.

Below is one example of the first page of a vehicle leasing business without about 1,000 trucks and vans under management. The Director of Finance explained he wanted a format that would resonate with each site manager throughout the six-store chain. The most important question was, “What’s important to the managers and the CEO’s leadership team?” While the excerpt below only shows the front page, a similar analysis follows over the following 15 to 18 pages.

Developing meaningful financials is part art, part science. By making the numbers more compelling to read, financial statement readers will make quicker and more informed decisions based on the analysis they are being provided.

There Will Still Be Obstacles

I can teach accounting managers and controllers this process in a few hours. We can have a system rolled out in less than one day. Unfortunately, the biggest obstacle to change is that the accountants liked what they were doing before. Creating new behaviors is not easy.

Competence is not an impediment. It’s a culture change. One of my $40 million clients was used to third-week-of-the-month financials for years. While training only took a few hours to teach the above process, the culture had to be changed. This company churns out numbers in three days each and every month. Needless to say, the CEO is extremely happy.

What does your financial closing process look like? Is it leading to better and faster decision-making? Do you have standards in place for timeliness? Accuracy?

How about your reporting format? Does the CEO fully understand what he/she reads with minimal effort?

The secret to financials in 3 to 5 days is a checklist. The other secret is getting started and developing the habit of following the checklist.

It’s your turn. Here’s what I want you to do:

- Download your COA into a spreadsheet.

- Add a column and name it maintenance.

- Go through all balance sheet accounts and state how you maintain those accounts.

- Do the same for the P&L accounts (mainly for revenue, COGs, and R&M).

- Add another column for month-end closing procedures.

- Quit being a perfectionist – focus on the content, not the form.

- If you work with a financial management coach, never ask for a copy of an old template. That’s shortcutting the learning process. Complete the steps above, and the coach can help you fill in the gaps.

And if you are still stuck, reach out for support.