I’ve always hated journal entries (JEs). Fellow controllers with deep backgrounds in technology and operations management know where I’m coming from. But how can I say this when the purpose of a JE is to true up an account to a complete and/or accurate state? Without such entries, the general ledger would be inaccurate, right?

I’m Including JEs and Adjusting JEs In This Conversation

Not all journal entries are the same. I live in Columbia, MO, and one of our retail crown jewels is the Pierpont General Store. I estimate they generate less than $1.5 million in revenues annually.

I’m 99% certain their POS data is not linked to their general ledger. Accordingly, a clerk likely creates a daily journal entry to record sales and estimate the cost of goods.

In a similar vein, payroll entries fall under this category, as operational activities must be recorded. Every small business should always outsource its payroll. Accordingly, when payroll occurs, we need an entry to book salaries, payroll taxes, and benefits. If not, expenses and cash are understated.

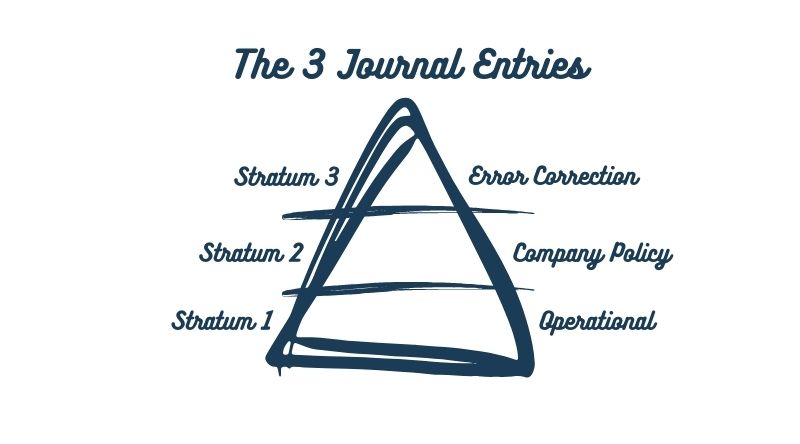

I call the above entries Stratum 1 entries. They are operational in nature and must be recorded because automation does not exist, or the operating systems that generate these transactions are not tied to our general ledger.

The next type of journal entry is based on corporate policy or our own accounting governance. My favorite example is in the eCommerce world, where customers return products for a refund or a replacement. Accordingly, managers may deem it necessary to record a 3% monthly levy on sales for returns and allowances. I’m calling this a Stratum 2 entry.

Finally, there are Stratum 3 entries used to fix errors. Let’s take the Stratum 2 example above, where the auditors pressure-test the adequacy of the reserve for returned merchandise. Assume their analysis reveals a 2.5% reserve should be applied based on past customer behavior on returns. Furthermore, assume that the reserve is roughly $250,000 overstated, a big cookie jar that surpasses the auditors’ materiality threshold. The entry they would make would be an error correction.

Many small businesses with revenue under $2 million have many of these Stratum 3 entries, which accountants call adjusting journal entries.

If we stop right here, the young bookkeeper might be thinking, “So it’s adjusting entries Mark hates.” That’s still incorrect. It’s all journal entries.

I Will Leave You Hanging

My goal as an executive financial advisor is to get CEOs to think about their thinking. That’s hard to do with young accountants or outsourced bookkeepers, because, in my experience, many want the quick answer so they can move on.

However, I’m going to stop here to let the young accountant figure out why I hate journal entries. I’ve left all the clues in the writing above. Most controllers I work with come from a public accounting background, and they know where I’m coming from.

However, I will leave one more hint in the form of a maxim:

Journal Entries

In general, the larger the company, the fewer the journal entries in the general ledger, especially those in Stratum 3.