After reading a Jeff Walker post on his personal blog, I learned about an organization called Write to Give. In short, Write to Give enlists elementary school students to write books with proceeds going to children in developing nations.

What a great model for all involved. And a huge high five to the founder of this organization, Amy McLaren (you can learn more about her work in this interview).

Can The Write to Give Model Be Replicated Locally by Nonprofits?

Over the past twenty years, I have volunteered for several non-profit organizations and served on four different boards. And here is one truism that applies to all nonprofits: raising money is hard, really hard. Fulfilling the mission is generally heartfelt and even comes across as easy for these organizations as they serve unmet needs for their constituents.

But raising cash? Complicated, frustrating, daunting, tiring. I’m running out of words.

What Are the Silver Bullets for Raising Cash?

I wish I knew the secret to finding an endless supply of cash for every non-profit I care about. That’s why I appreciate Amy’s creativity in getting young kids to write books to feed the minds of children around the globe who desperately need an education.

While I do not possess that silver bullet for alleviating budget shortfalls, Amy’s idea reminds me of an important concept when raising funds in the nonprofit arena. That concept focuses on high-return activities that require minimal effort.

I’m sure Amy worked hard at executing this project. However, I assume the subsequent cash-generating activities became somewhat easy once the system was built. No, this endeavor is not generating hundreds of thousands of dollars, but I’d still characterize this cash-generating idea as high-return with minimal effort.

High-Return, Low-Effort Fundraising Activities

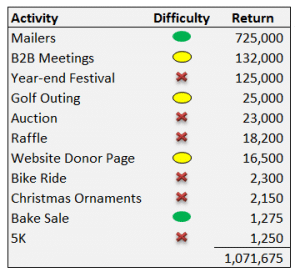

One of the best exercises any executive director can perform is to list every channel or source of contributions from donors. That list should also include a column for the level of effort. In the image at right, I’ve listed 11 fundraising activities for a fictitious non-profit organization.

Your determining factor for difficulty could be the number of hours expended by either staff or volunteers. Difficulty could also be based on frustration levels. You decide how to use this column.

For return, use gross margin dollars, not gross contributions. I’ll explain why later on.

As you work on this exercise, consider adding columns for staff hours used and volunteer hours.

Another potential column to add is Positioning. For example, the 5k event appears to be a low-return, high-effort activity. But if the run attracts nearly a thousand participants, you gain exposure for your organization.

If this is the first time you have attempted this exercise, keep it simple for now. Listing the two columns will give you and your team valuable insights.

Takeaways from Identifying High-Return, Low-Effort Activities

Just because you yield a high return on one of your fundraising activities doesn’t mean you have a winner. If the level of effort is high and frustrating, it’s time to rethink how to employ that particular fundraising activity in the future.

Let’s pick on our 5k example again. These events can seemingly be a big deal for non-profits. I’ve run in many where the participant level was 800 runners. Even if the return is high, staging an event like this requires much work and many volunteers. This is nearly a full-time job for an event coordinator during the two or three weeks leading up to the event.

In a case like this, I wouldn’t toss the 5k. Instead, I’d consider having someone else run the event. The return may be lower, but the level of effort is lower, freeing up valuable staff and volunteer time to work on higher returns and lower effort activities.

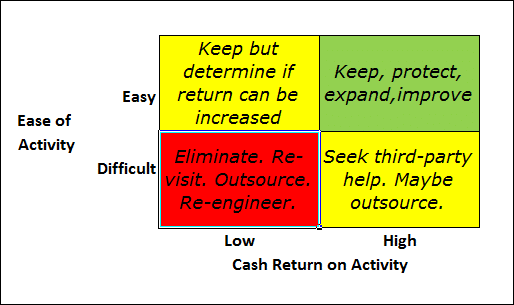

Accordingly, the biggest takeaway of this exercise is that the executive director and his/her team are now thinking about every fundraising activity strategically. Consider the following matrix. In the following boxes, consider what the strategy should be in each quadrant.

Your answers will be different. Suppose you assign every fundraising activity to one of these quadrants. In that case, your frustration levels will drop as you spend more time working on the events and activities that return the most significant cash at the lowest effort.

Do Not Focus Just on Fundraising Dollars

I think the budgeting process is the most significant waste of time in any non-profit organization. Budgets are usually obsolete by the end of the first or second month of the new fiscal year. Instead of revising the budgets each month, I continue to hear explanations of what is causing variances, as though that is the objective.

A far better approach is to re-forecast every month using what-if scenarios and various stress-testing techniques. The executive director and his/her team in the back office should do this, and it should be front and center in every board meeting when finances are discussed.

However, we live in a non-profit world clinging to its budgets. And if that’s the case, you have to get out of dollar-mode-only thinking when it comes to fundraising.

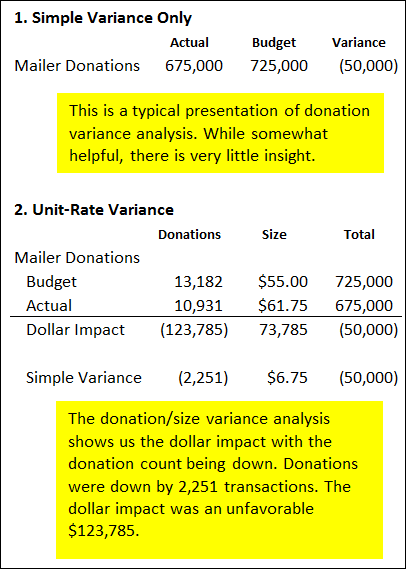

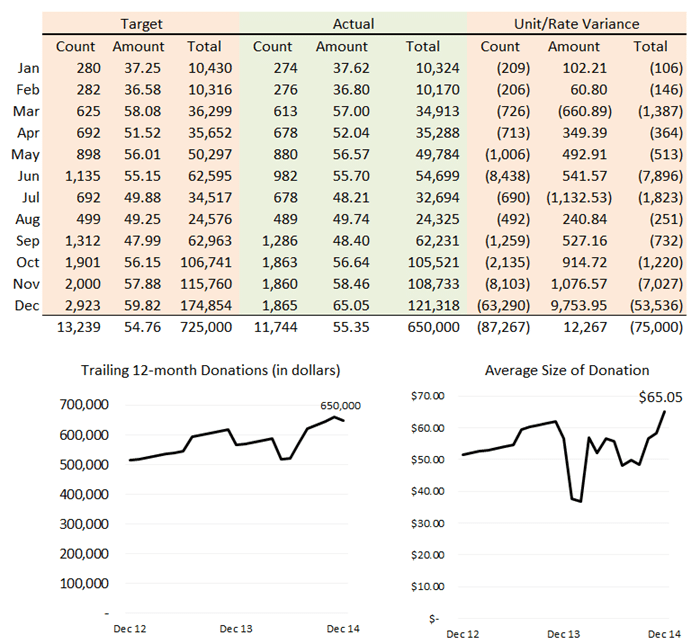

Let’s take a super simple example–mailers. Let’s say the average donation is $55. If you generate $725,000 from your mailers each year, more than 13,000 generous donors send you checks each year.

So if the budget is $725,000, what if you only collected $675,000? That’s an unfavorable variance of $50,000. What does that mean? Why the drop?

The snapshot at right shows two simple presentations showing variances from budget for mailer donations. The top example is how most executive directors present their monthly/annual numbers—actual, budget, and variance. Talk ensues, and a plan is made to do better next time.

Now consider the second presentation. At first, this won’t be very clear. But let’s review this by answering the following question: What was the dollar impact of the number of our contributions exceeding or underperforming the plan? Remember, you need to budget not just dollars but transaction counts, too. Next, what was the dollar impact of the average check exceeding or missing the budget?

In my example, the donation count was off by 2,251 transactions (the simple variance row). That drop unfavorably impacted our budget by $123,785. Our average check was $6.75 higher than planned, which favorably impacted our budget by nearly $74,000.

So, which analysis is better? Which analysis provides the most insight? The second presentation.

We’re still not done, but at least we know where to begin our work to increase our mailer donations.

Raising funds requires two strategies. One is to increase the number of donations we receive, and the second is to increase the amount each donor gives us. This simple analysis tells us which strategy to work on.

Don’t Forget to Focus on Gross Profits

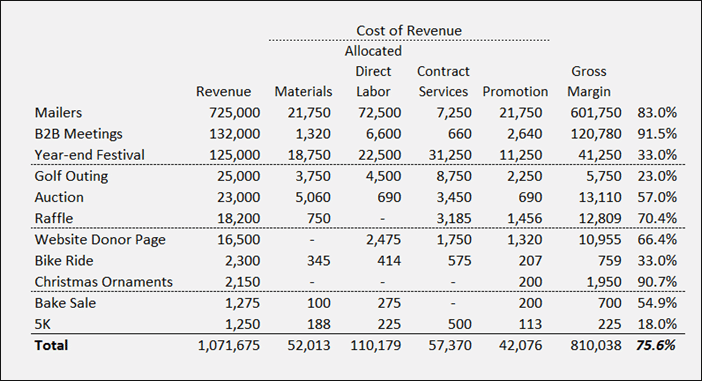

I’ve looked at scores of non-profit financials. I’m amazed at the lack of reporting regarding gross margins. Nearly every fundraising event has direct costs closely associated with the dollars received from donors. You have to know those direct costs.

In our mailer donations example, the direct revenue cost is minimal. Postcards and postage are the overall cost, which is probably $1 to $2 per unit. Expressed as a percentage of donations received, the gross margin is probably well over 80 percent.

In contrast to large annual festivals and sporting events, the gross margins are probably closer to 30 to 40 percent, a big difference. Low margins do not mean we need to eliminate the activity. We cannot believe that all large-donation activities are highly profitable.

In short, know thy gross margin on every fundraising activity. If you are not doing this, make sure your reporting and budgeting process provides insight into your gross margins as shown in the example below:

Final Fundraising Thoughts

I admire what Amy is doing with her organization, Write to Give. Using kids to help other kids is very fitting.

I do not know all the facts, but Amy’s idea caused me to conceptualize the return on fundraising activities and the ease or difficulty level of obtaining those funds.

So let’s review our checklist of activities in the future:

1. If you are an executive director, a board member, or a volunteer, can you characterize every revenue-generating activity, the total return, and the difficulty level to obtain these contributions?

Have you decided which activities should be cut, modified, or enhanced?

2. We analyzed how you should look at your variances from plan or target. We need to focus on transaction counts as much as we do dollars. We manage activities; we count dollars.

This method presupposes you budget your donations not just in dollars but by the number of donations and average transaction size. Each month, you should update the variance analysis we showed, which will help you determine specific strategies for attacking weaknesses in your fundraising activities.

While overly simplistic, the dashboard below will help you to think through this process:

3. Finally, you cannot just focus on top-line contribution dollars. You have to look at the cost of donations by each fundraising activity. Gross margin analysis is not just for the corporate world. Nonprofits need to focus on gross margins, too.