Looking for a way to shave some dollars off your line of credit interest?

This is not for the faint-hearted, but it’s effective. Additionally, you’ll need a pretty decent finance person at the helm to pull this off. Oh yes, not sure what LIBOR is? Then this CFO hack is not for you (yet).

4 Steps to Short-Term LIBOR-Based Financing

1. First, I’m assuming you have a bank that offers alternative pricing based on the London Interbank Offered Rate (LIBOR). For example, if you bank with Wells Fargo, they offer both prime and LIBOR-based rates.

So step 1 is asking your banker if they offer these rates. Many small community banks do not.

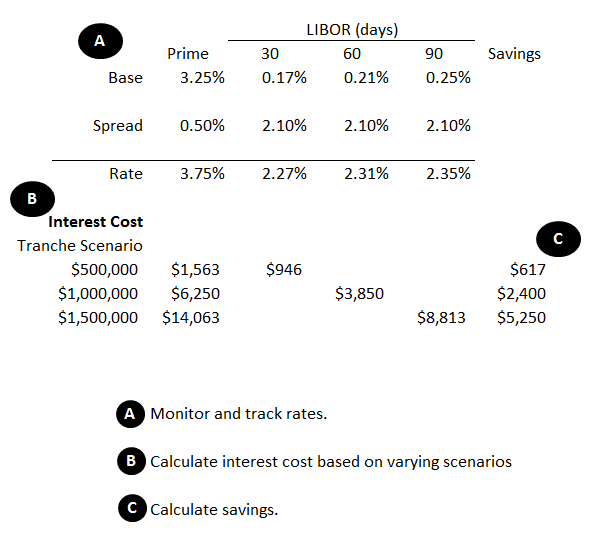

2. Track the current LIBOR rates. You can monitor these rates at Bankrate.

Generally, the short-term LIBOR rates will be lower than your current prime-based line of credit interest rate. So it’s always good to know the spread between these two rates which is specified in your revolving loan agreement.

And the next logical step is to compare your post-spread rates with one another. I’ve shown an example of this at the bottom of this discussion.

3. Here’s your X Factor–forecast your short-term line of credit balance.

You have to know your projected line of credit balance as we’ll be fixing your LIBOR-based note over (generally) three or six months. We do not want to be paying interest if we believe our line of credit is going to be minimal or have no balance at all.

My plain and simple advice–don’t do this if you do not habitually maintain a rolling cash flow forecast. The best controllers I know do this weekly. If so, that’s the analysis you’ll use to make your decision.

4. If projecting the line of credit balance is the X Factor, estimating the interest savings is the fun part.

Let’s do some simple math assuming your short-term rate is 3.75 percent (50 basis points over current prime). We’ll assume we know we’ll have an average LOC balance well over $1,000,000 during the next 90 days. So let’s say we divert $1,000,000 from our prime-based LOC to a fixed, 90-day LIBOR note …

Prime-based – $1,000,000 * 90/360 days * 3.75% = $6,250 interest expense

Now let’s assume our LIBOR-based pricing includes a 210 basis points spread with a base rate of .25% …

LIBOR-based – $1,000,000 * 90/360 * 2.35% = $3,850

In the scenario above, converting $1,000,000 to a 90-day fixed LIBOR note would yield a $2,400 savings. Repeating this process throughout the year on higher dollar amounts leads to some decent cost savings on interest.

To LIBOR or Not to LIBOR

If your bank offers LIBOR-based funding and your bank line of credit is easily predictable and significant, the risks are essentially non-existent. The key is good predictability with your short-term cash flows.

Below is a screenshot of how I do this, but I lopped off the 180 days in my example for better readability.

{kind=link}

Photo by Yong Hian Lim