I came from a corporate world where debt was expected and even planned. And that corporate world taught me it was okay to maintain a certain debt to capital ratio at all times. And for my larger clients, that works. Or rather, we make this manageable.

In smaller businesses, especially with revenues under $10 million, debt can be a killer. Many business owners I’ve worked with over the years have needed money immediately for additional working capital, maintenance capital expenditures or for expansion.

Many of these business owners sign on the dotted line a little too quickly, and all is well until that first debt payment. And then the second. And the next.

Life just got hard, complicated, and stressful.

A Simple Debt Tracking Tool

{kind=link}

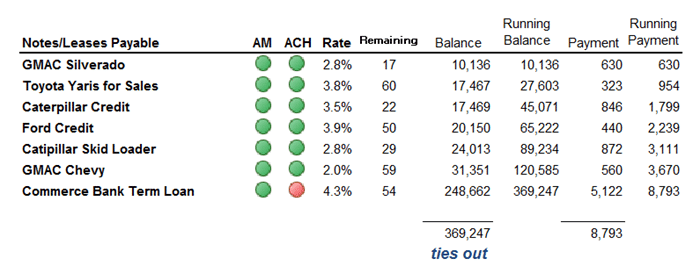

When I work with a small business that has a large chunk of debt on their balance sheet, the very first thing I do is create a schedule of every balance owed to a bank, lessor, or any other lender. Here’s an example of what I’m talking about: In the first column, I list out the type of debt. Usually, I’ll even include another column showing the purpose of the indebtedness.

The next two columns are abbreviations for amortization schedules and ACH payments. I always create amortization schedules for each debt instrument. And my preference is that every loan payment is paid automatically and electronically each month, no exceptions. I then want to see the interest rate for each note in case I need to refinance a high-priced loan.

The next columns show the total balances on each note (my sort order is low to high) along with the monthly payments. The last column shows the cumulative total of debt payments each month. In the example above, the small business owner is making payments of $8,793 per month.

Notice the note at the very bottom of the balance column. I always make sure the total balance ties out to the general ledger. Care to guess how often these numbers tie out when I first do this analysis for a small business owner? Rarely.

A Few Takeaways from This Simple Debt Schedule

A few years ago, I worked with a small business doing about $1.3 million in revenue. The husband and wife worked closely together and made a great team along with the family dog. Debt was a major source of stress. So I created a schedule similar to the one above, although the list was much longer and the balances were higher.

Creating the schedule did not make the debt disappear, but here’s what happened:

- Eyes were opened. The couple knew they had a lot of debt. But now they saw the big picture on one piece of paper (actually in Excel, but ‘paper’ just looks better in writing).

- And this (new) heightened sense of awareness led to confidence. The stress of making payments still existed, but now they began to realize this debt snowball could be managed and ultimately whittled away.

- And this renewed confidence led to a plan–using excess cash to slowly eat away at the debt balances.

In some cases, this couple had 0.00% interest on some of the notes. However, they largely ignored this variable and generally knocked out the smaller balances in order to free up cash flow.

They didn’t necessarily use that new-found cash to immediately ramp up payments on the other balances. Instead, we forecasted cash carefully making sure we had enough money in the till to address unexpected surprises. Only after that exercise would we start accelerating payments on the next smallest balance based on our forecasting insights.

Such a simple tool, yet much financial intelligence was gained for the small business owner. And did I mention the schedule only took about an hour to complete?

The Final Takeaway Is Knowing What You Can Afford Under Multiple Scenarios

The final takeaway is that we learned quickly the number of debt payments we could afford each month. In their case, the debt load led to stress. So we ran multiple scenarios to determine a good mix of free cash flow to debt payments.

Personally, I shoot for free cash flow to debt service of between two to three times. That is, I want my free cash flow to be two to three times in excess of the total principal and interest payments over the course of any 12-month time period.

Obtaining the right mix may take two to three years to achieve, but fixating on healthy cash management habits will lead to a discipline that meets the desired target.

I know, my recommended ratio seems high and maybe foolishly too conservative from your point of view. Remember, I stated, “shoot for.”

Start-ups, that ratio will be really tight (unfortunately), like closer to one to one. Growing companies, that ratio may be closer to 1.5 to 1.75. And that means there is little room for error. If sales start going flat or southward, a cash crisis will certainly follow.

The bigger point is that I focus more on ‘what can we afford?’ vs. what the debt-to-capital ratio looks like. I want cushion or peace-of-mind cash flow margin for my clients.

Small business debt is certainly a necessary evil in any small and growing business. But at least we now have a process for managing these debt levels that will lead to more confidence for the financially-intelligent business owner that had otherwise been operating in the dark.