I am thankful for the new Federal income tax laws that allow pass-through entities to deduct state taxes as any other ordinary expense. That number can be significant and a lovely gift from Uncle Sam.

However, I was shocked when I saw how smaller businesses started reporting this on their income statements. Am I surprised? No, but I’m disappointed because the internal accountants were (and still are) allowing the tail (tax reporting) to wag the dog (meaningful management reporting).

I’m going to let you in on a secret. Even small business CFOs and controllers find the concept confusing, so they take the path of least resistance by following the advice of external accountants on reporting the newly allowed deduction.

In this brief discussion, I will explain how pass-through state income taxes should be reported in the financials each year.

The Three Reports

Before I address the proper internal reporting for pass-through state income taxes, we need some foundational thinking about reporting in general. If you are subject to audited reports, every U.S. business has three bases of reporting:

- Meaningful (internal) management reporting should be done using the accrual method for accounting purposes.

- Tax basis (which could be cash or accrual).

- GAAP basis.

The following video content will still apply if you are not subject to GAAP reporting, but the reconciliation process will be quicker.

In summary:

- At a minimum, every small business has internal and tax reporting. Those subject to external reviews and audits will have a third reporting basis for GAAP.

- The three reports should never have the same bottom lines or net book value (NBV for equity).

- All three reports should be reconciled annually.

Departures from Tax and GAAP Reporting – A Few Examples

Instead of trying to write about examples where the three bases of reporting depart from one another, let’s do this through a quick video:

All three reporting bases will reveal different numbers for depreciation expense and the net book value for all fixed assets. The three forms of reporting will differ for owner health benefits and possibly officer compensation (depending on the tax partner’s compensation strategy for the owner).

While the numbers are smaller, permanent timing differences occur with meals and entertainment, tax-exempt interest on muni bonds, Federal tax penalties, and life insurance proceeds on an officer’s life insurance policy, to name a few.

Over the past 20+ years, I’ve punted on some odd GAAP accruals hitting the audit report. I refuse to book an asset and liability for a real estate lease. While I’m departing from GAAP, it’s easily reconcilable. Also, I’ve never had a banker challenge our internal reporting convention.

Again, differences between internal reporting, GAAP, and tax are typical. That’s why we reconcile these numbers annually.

The Smart Way to Report Pass-Through State Income Taxes

In cases where I own the reporting, I report pass-through entity state taxes as a distribution. Before the pass-through entity deduction, nearly 100% of the owners I worked for paid their federal and state taxes through business distributions, an equity transaction. Those transactions never hit the P&L. That practice should continue.

Because of the new deduction allowance, I’d make that number ‘more’ visible on the detailed balance sheet by adding an account entitled Distributions – State Taxes. It’s still a distribution, but I’ve called it out with this new account.

GAAP will reveal the expense between EBT and Net Income. However, my internal reporting on the balance sheet will still tie out to the GAAP reporting as both reduce equity.

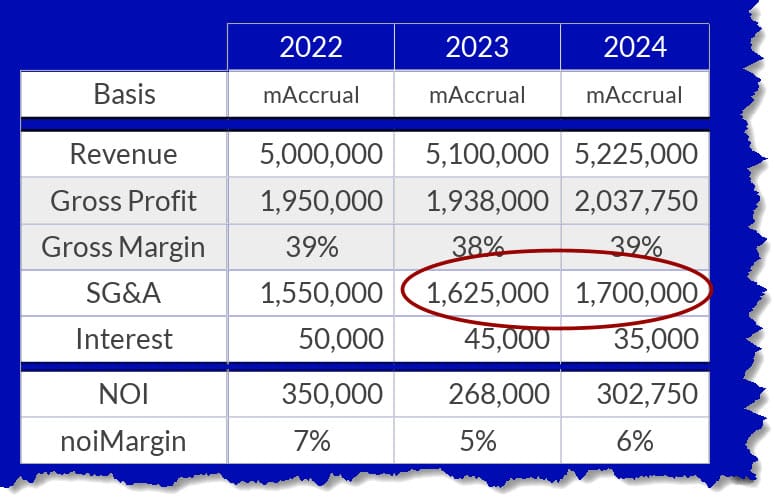

Several small business owners I have worked with are lumping this new expenditure in SG&A, which looks foolish. In the example below, the internal accountant recorded the pass-through tax in SG&A starting in 2023 for no reason other than the guidance they got from the tax partner. Is that the only reason to record the number in the general ledger as an expense instead of a distribution?

For business owners only, just because your accountant books an entry to a distribution doesn’t mean the outlay is not deductible on the tax return. It is. Remember from the video earlier that we reconcile the numbers annually? Our bases of reporting should never be equal, but they are reconcilable.

Incidentally, if you are guilty of recording the expense on the P&L, what will you do when the IRS no longer allows this pass-through entity deduction? It could happen.

While you’ll stop recording the expense, my clients, with strong financial reporting acumen, will still run their distributions through equity, as state taxes will still have to be paid. Under my method, nothing changes. We had meaningful reporting before and during the new law and will continue if this deduction is repealed. Consistency will be a constant.

What Happens When My External Accountant Disagrees With Me?

External accountants do not own your internal trial balance. The better question is, “Why are they so focused on their way of reporting?” That’s easy to answer:

- Tax accountants look at your numbers through their lens or prism. Naturally, they expect you to report numbers that make their lives easier. We do so through that special distribution account we created.

- External auditors believe the world revolves around the GAAP report. Until those external auditors become CFOs and controllers, they will never appreciate the meaningful reporting a CEO craves. I will never throw them under the bus because their hands are tied to their GAAP bible.

- Internal accounts know that life revolves around the business model of finding, getting, and serving a customer. All reporting syncs to that business model through healthy corporate and accounting governance, which typically depart from tax and GAAP reporting.

In short, all parties view the world differently from a reporting standpoint. However, we must still reconcile the numbers while achieving all three reporting purposes.

The Rational For My Reporting Standards

The purpose of a business is to find a customer, obtain a customer, and serve a customer. All reporting should reveal the results of making that happen.

Yes, we have compliance reporting requirements for Federal and state income taxes, sales taxes, and external GAAP reporting, among other documents required by third parties. But that doesn’t mean we cannot run our internal financials using modified GAAP conventions that easily tie to the ‘real’ GAAP and tax numbers.

If you choose to be a slave to tax and GAAP reporting, that’s a step back from the original reason for even being in business–loving your customers. GAAP and tax reporting should not dictate intelligent business reporting. The business model should. Just be wise about how you do so.

Appendix: Remember PPP?

I’ll never forget the day I reviewed the P&L of a temp staffing firm based outside of Dallas. Other income included the forgiveness of $1.3 million in PPP money and radically elevated that year’s net income.

“What’s this?” I asked the owner. I knew the number and wanted to hear the owner explain it.

Net income was ridiculously high compared to the skinny profit margins they had lived on for the previous three years. That money saved them, and they loved seeing that bottom line.

But I wasn’t fooled.

GAAP accountants, you are correct that loan forgiveness lives on the P&L. But how do you think I recorded the PPP forgiveness for businesses I work closely with? A few CFOs liked my idea but were afraid to follow the book on debits and credits. Too bad.

I parked the forgiveness money directly into a special Paid-In Capital account. Under both methods, equity ties. But my method removed the illusion that “We had a great year.” No, capital increased because Uncle Sam said, “Here, take this.”

Should Everyone Book the State Pass-Through Deduction on the Balance Sheet Only?

The short answer is “No.”

For the owner running a small lifestyle enterprise that is more concerned about cash in the bank and heavily focused on reducing taxes, I’d allow the tax people to decide where the deduction gets reported in the owner’s accounting system. Obviously, they will have the owner expense it.

As the business grows, so will the owner’s financial acumen. He/she will probably have a controller or finance VP on the team. This organization releases the month-end reporting one to two days later and reviews a well-designed, actionable reporting package that pairs with its rolling financial model. I don’t have research to support this claim, but I bet more than 75 of these businesses run the deduction through equity, as described above.

Smaller business owners with checkbook-like financial acumen can follow the guidance of tax accountants. As the sophistication of the leadership grows in the business, the norm should be, “Don’t expense.”